For most of us, when we are young and carefree, the last thing we are thinking about is our financial future. Life moves slow and we have all the time in the world!

The older folk may tell us “start investing now while you’re still young” which goes in one ear and out the other. We have more important things to do… Right? Wrong!

While it may seem like an overstatement, starting now vs starting in 20 years may the difference between a comfortable vs financially stressful retirement.

WHY is it so Important to Start Investing Early?

The importance of investing early can be summarized in two words: Compound Interest.

Albert Einstein once quoted: “Compound interest is the eighth wonder of the world. He who understands it, earns it; He who doesn’t, pays it.” Earning it sounds much better than paying it, so we better understand it!

Before digging into compound interest, let’s look at the first step of the equation: Simple Interest.

Simple interest is the interest earned or paid based on the original principal (amount loaned or borrowed).

As an example, you put $10,000 into a 3-year CD with your bank that pays an interest rate of 3%. The interest payments would be as follows:

- Year 1: $10,000 x 3% = $300 interest

- Year 2: $10,000 x 3% = $300 interest

- Year 3: $10,000 x 3% = $300 interest

These interest payments received are an example of simple interest.

Each year, you will be paid the same amount of interest. The interest payments don’t change because they are always based on the same principal amount.

Compound interest adds another factor into the mix, and this is where the magic happens. While simple interest is only based on the original principal, compound interest is based on the sum of the original principal AND all the previously accumulated interest. The interest “compounds” on itself, and allows it to grow exponentially.

As an example, let’s say you put $10,000 into a high-yield savings account paying 3% annual interest. If you leave all the money in the account, including the interest, here are your payments:

- Year 1: $10,000 x 3% = $300

- Year 2: $10,300 x 3% = $309

- Year 3: $10,609 x 3% = $318

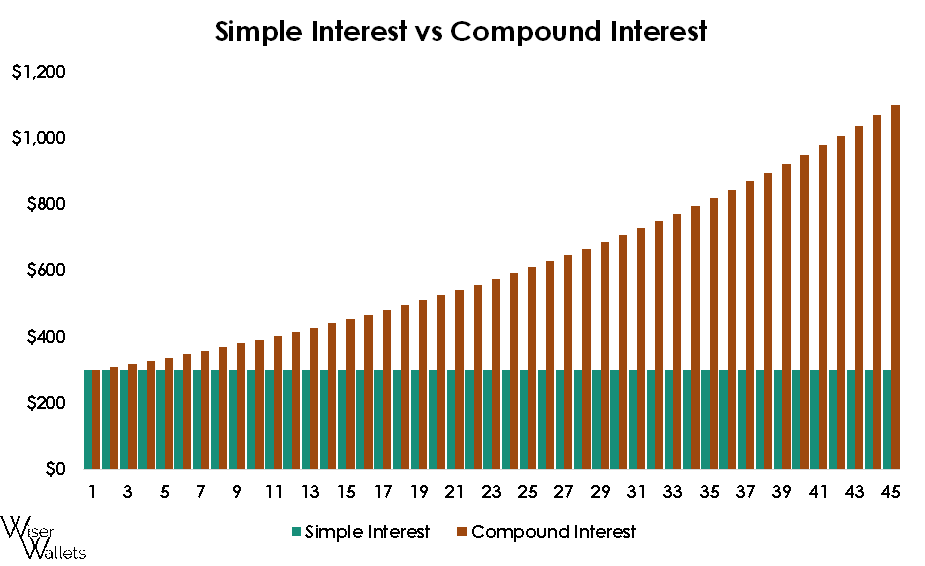

The chart below shows a visual of the same example over a 45 year period. As you can see, the simple interest stays the same over the entire period, while the compound interest grows exponentially.

At the end of the 45 year period, the simple interest is still $300 per year, but the compound interest has grown to over $1,100 per year!

While this is a relatively small scale example, let’s look at an example that is more realistic from a retirement savings standpoint.

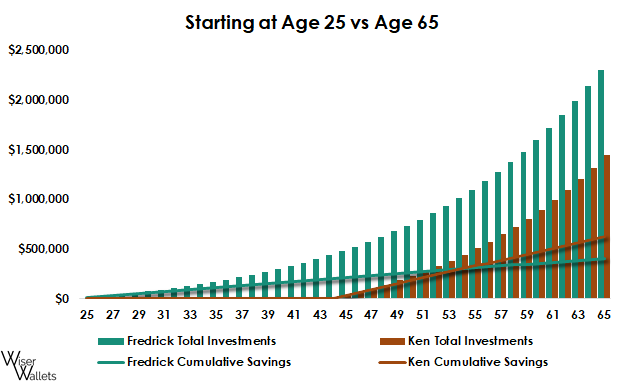

Fredrick is 25 years old. He was fortunate enough to understand the power of compound interest early in life, and is taking advantage of the opportunity to start saving a relatively large portion of his income and investing it into the stock market. He has started saving $10,000 per year, collectively, through his employer 401(k) and Roth IRA.

Ken is 45 years old. He has worked very hard in his career to support his family, but saving for retirement has never been a focus, and he has fallen behind. Realizing this, Ken and his family cut down on expenses, and Ken begins putting $30,000 per year, collectively, into his employer 401(k) plan and IRA.

Let’s assume both Fredrick and Ken grew their investments at an average of 7% per year. Fast forward to age 65…

- Fredrick, at age 65, has accumulated about $2,300,000

- Ken, at age 65, has accumulated roughly $1,400,000

While Fredrick has accumulated a greater amount than Ken, consider the following:

- From age 25 to age 65, saving $10,000 per year, the cumulative amount Fredrick has saved (not including the interest earned) is $410,000

- From age 45 to age 65, saving $30,000 per year, the cumulated amount Ken has saved (excluding the interest earned) is $630,000.

In essence, Fredrick did a greater job of leveraging the power of compound interest. By using his young age to his advantage, Fredrick saved about $200,000 less than Ken in total, but ended up with almost $1,000,000 more by age 65! This example is illustrated in the chart below:

Starting young allows for more risk and potentially higher returns

Starting young also provides another key benefit that can greatly enhance returns over the long-run – the ability to take on more risk.

When you are in your 20s, 30s, or 40s, you generally have a longer-term investing time horizon relative to someone who is retired, or close to retirement.

The benefits of having a longer time horizon is that you can invest a greater portion of your money in more volatile securities, such as stocks or real estate.

You won’t need to use the money for many years, so you can absorb the volatility much better than someone who is retired and is living off their investments. While these investments can fluctuate greatly in value, you are generally rewarded more heavily by higher returns.

Now that you understand why it’s important to start early, the next question may be WHERE do I start?

Hopefully at this point, it’s clear to you that starting as early as possible is the best path for your long-term success in investing.

But how do I get started? What if I don’t have the “extra funds” to set aside to invest? (Spoiler alert… “Extra” money doesn’t exist). If I carry debt, should I pay that off before investing?

For a detailed breakdown on the steps to take and what actions to take first, check out this blog post to get yourself headed in the right direction.

Investing doesn’t have to be complicated. A great first step to take may be to start contributing to your 401(k) plan, if you have one. Most employers even have a matching contribution, and not taking advantage of that is leaving free money on the table.

Additionally, setting up an IRA or a Roth IRA is another great way to invest while also taking advantage of available tax benefits.

Many people (myself included) set up automatic monthly withdrawals from their bank account into their IRA or Roth IRA, so you don’t have to remember to do it manually each money.

I prefer this “set-it and forget-it” approach because it allows you to get comfortable with not having that income at your disposal each month. This is an extremely powerful tool for taking advantage of long-term compounding.

What if I am already in my 40s or 50s, and I still haven’t started saving?

Maybe you have already passed your younger years, and you are just now starting to save. While starting young is a huge plus, if you no longer have time on your side, there are still some things you can do to try and catch up.

First and foremost, DO NOT take on additional risk to try and “catch up” and offset the returns you missed out on. The chances are, this will leave you in an even worse spot. Stay true to yourself and take on the amount of risk that you are comfortable AND capable of taking.

If you have access to an employer 401(k) plan, take full advantage of any matching contributions, and do your best to make the maximum contributions you can to the plan.

If you are 50 or older, you can make additional “catch-up” contributions to your 401(k) that can further spur your savings.

Other tax-advantaged accounts to consider using are HSAs, IRAs, and Roth IRAs. Taking advantage of tax benefits when possible can help grow your wealth faster.

The key here to remember – as illustrated in the Fredrick and Ken savings example above, due to absence of savings earlier in life, you will need to save a greater amount now to try and catch up as much as you can. But don’t take on too much risk to try and offset the years you missed out on.

Reviewing your expenses and cutting down on unnecessary costs can help free up cash flow for investing. If you are having a hard time prioritizing saving, and need some ideas on how to free up some income and save more, check out this blog post.

Start now, thank yourself later

We all want to be comfortable in our retirement years, but without creating a plan, and most importantly, taking action, your dream is just that – a dream.

Investing is not as intimidating as it may seem. Even if it were, it is such a crucial decision to make, that it literally may determine how financially comfortable you are in your retirement years. There is no reason to wait.

If you are still young, time is on your side – USE IT! Even if you are middle aged and still haven’t prioritized your financial future, start TODAY! It’s never too late to start.

As the old Chinese proverb says, “The best time to plant a tree was 20 years ago. The second-best time is now.”

Disclaimer: This blog post is intended for educational and informational purposes only and is not to be taken as investment or tax advice. Speak with your financial advisor before making any financial decisions.